Insider tip: Gold as equity for financing

Almost always the advice is: Sell shares and gold if you want to finance a property (or any other major purchase). That way you have the required equity. Right or wrong?

From the very beginning, this has felt wrong – or rather suboptimal. When the first building was to be financed in the middle of the financial crisis in 2008, that was the bank’s instruction. Selling shares at rock-bottom prices in the middle of a crisis? Financial institutions do such things with capital entrusted to them by customers, as hundreds of thousands of share-based Riester contracts prove.

If you want to lead an exceptionally financially successful life …

… you have to say goodbye to universally valid financial advice that is available everywhere for free or via regulated fee-based consulting.

This article documents how to contribute gold shares, gold ETFs, gold certificates, gold bars and even Krugerrand gold coins bought or inherited years ago as collateral for fresh money from the bank – without selling them!

For loyal newsletter subscribers, parts of this article are nothing new. Nevertheless, this will reach far and in some areas go into great detail so that you can replicate this strategy exactly. Perhaps there will be an opportunity to provide guidance along the way. For that, however, you need to be a bit special. See further down.

When the Goldvreneli coins were purchased, they cost just over 200 euros per coin. Today the bank grants a credit line of 432 euros per piece (60% loan-to-value, ISIN: CH0002813837). Story and instructions on this page.

Main section

The financial system is sick – make use of it (to your advantage)

For some of us, life is about building wealth. That is more than buying one or several properties and having tenants pay them off over decades.

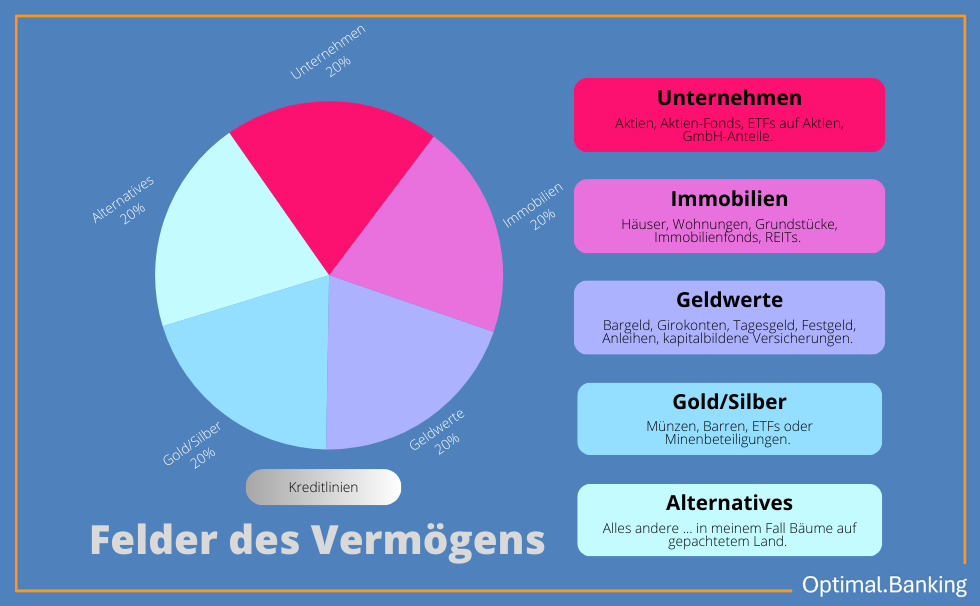

If a property portfolio of – to keep the math simple – 1 million euros has been built up, then according to old Jewish wisdom a further million each should be invested in businesses, precious metals, monetary assets and alternative investments. For this, the concept has been illustrated in the 5 fields of wealth:

Current positioning in 2024 can be found in this article.

The slow way would be to build this up in parallel. For example, via low-cost or (supposedly) free ETFs. Ideally with TradeRepublic, which will soon completely dispense with customer service.

Once a nice sum has been accumulated, the desire for a home of one’s own arises, and most of what has been saved is sold. As equity for the construction financing. What remains then? In the best case, truly a dream house, a monthly payment and a negative balance at the bank – plus a few ETFs. The intention is to build the ETF holdings back up again, but this proves difficult because the payment to the bank is a monthly burden.

It is clear that over the long term ETFs, funds or shares will yield significantly more than the bank financing will cost. For example, 7.5% performance compared to 3.5% loan interest.

Why are you doing this?

Because there was no better way known? This article changes that!

The simple part is: Do not sell the assets from up to 4 fields in order to grow in one.

The art is: organizing it smartly.

It is necessary to remember what real assets are and what monetary assets are (promises that are based on trust in a currency). Real assets are built up. Monetary assets are used as a means to an end.

Assets are creditworthiness

Assets are above all silent creditworthiness. Especially because credit scoring systems, above all Schufa, look exclusively at debt and consumption. Schufa has no way of recording assets.

It is even worse in the USA, where people are trained to consume heavily in order to have a good credit rating.

Yes, pay attention to a good Schufa score. At least know what it is. With silent creditworthiness, it is also possible to finance outside the Schufa system in such a way that Schufa does not see it. How this works becomes clear over the course of this major article.

Gold is freedom and can be a source of new money at the same time

Regardless of the current level of wealth building, gold should be owned. Gold must be owned when the level has been reached at which strategic relocation of assets to a safe foreign country is under consideration. Gold must be owned when wealth is to be built with the help of borrowed capital.

If the purpose of gold is not yet entirely clear, there is room to exchange views via the comments section. It is also possible to post some of the numerous knock-out arguments against gold and read the counterarguments.

For the further course of this article, let us assume that it makes sense to hold 1/5 of total assets in precious metals (see above). When the net worth balance sheet becomes larger and larger, the 1/5 in precious metals will also become larger and it might be a pity to leave that entirely unproductive for years or decades. Because gold in itself is unproductive. It pays neither interest nor dividends. Depending on storage, it even incurs costs.

Lending gold would be almost foolish in the current climate. Pledging it as collateral is another matter. It remains personal property. Only if the borrowed money cannot be repaid will the collateral be liquidated.

This is the requirement: to use the capital secured by gold in a meaningful and profitable way!

Concrete instructions

How to obtain fresh capital with gold in 4 steps

- Open a special securities account with one of the banks in Liechtenstein.

- Transfer the agreed amount or the start-up capital.

Alternatives: securities transfer or depositing already owned gold coins! Details further below. - Receive a credit line (= Lombard loan) at incredibly favourable terms that requires no disclosure and remains invisible.

- Use the fresh capital for investments that yield more than the interest costs (for example property renovation and furnishing of holiday apartments).

Regarding 1.) Opening an account in Liechtenstein

It is not possible to open just any account at any random bank in Liechtenstein. For the system to work, connections are required. The right ticket to the right banker at the right bank! This is the letter of recommendation if the requirements are met and there is a good understanding. The account can be opened in personal name, as a joint account or as a business account.

The account opening can take place in person on-site or by mail. If desired, additional banking services can be added. This is private banking. That means: service has a price. Service is of high quality. Things are possible that are unthinkable in Germany. Welcome to another world. Even if it is also German-speaking.

If there has not yet been personal contact, the process is: establish contact – initial phone call – decision whether to open the account by mail or in person – setup of the system.

If there has not yet been personal contact, the process is: establish contact – initial phone call – decision whether to open the account by mail or in person – setup of the system.

Regarding 2.) Lodging assets in Liechtenstein

With the account opening comes an LI-IBAN. From any German bank – or also internationally using the BIC – money can be transferred to the bank account in Liechtenstein. Transfers are possible in EUR, CHF, USD and some other currencies. The capital then sits in the account in Liechtenstein. For some, this is sufficient, because they simply want to bunker their “cash” safely and keep it available at all times.

In terms of the strategy of using gold as collateral to gain access to fresh capital, one option would be to use the transferred money to buy gold. This is something that was done already in 2009:

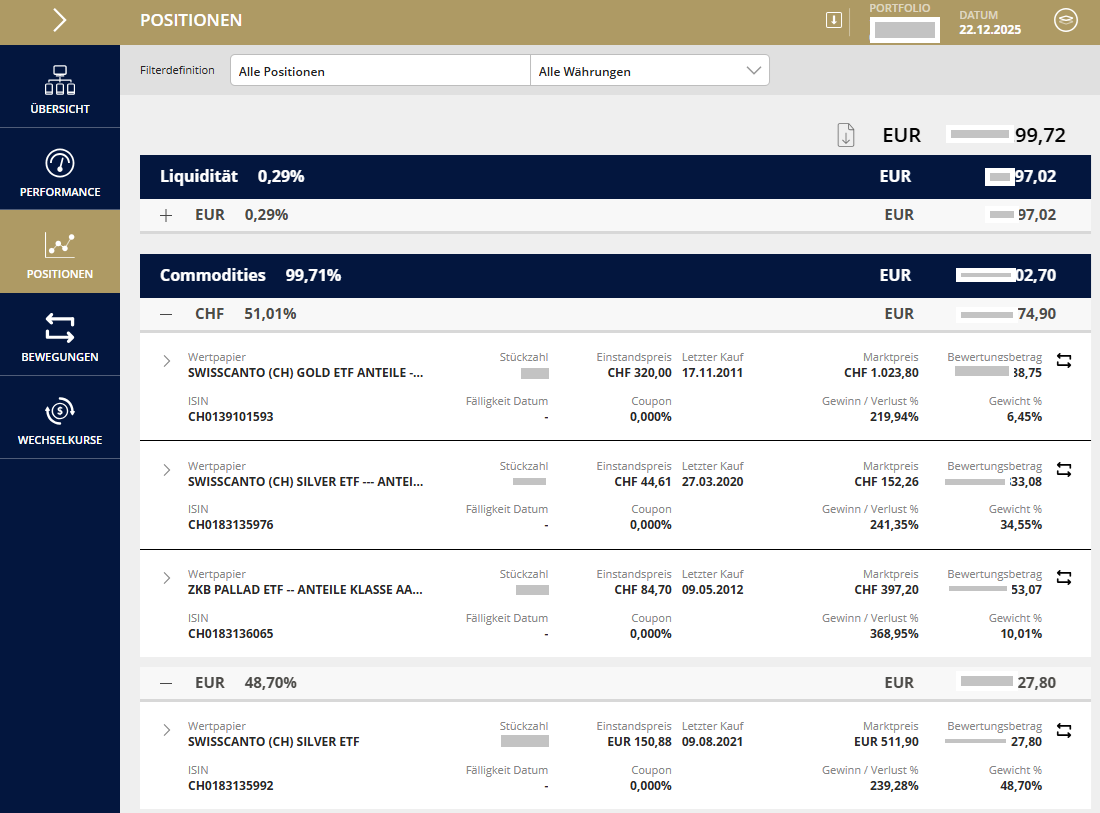

It is visible that not only gold, but also silver and palladium are held in the securities account via physically backed ETFs.

Bonds, shares, ETFs, funds?

They do not have to be precious metals.

There are also people who transfer their securities account with shares from Germany to Liechtenstein. This has two interesting advantages: a) dividends pay the loan interest and b) the securities account is hardly subject to seizure or freezing by current or future (EU) authorities. Keywords include EU asset register, distribution of future war burdens or other levies on assets.

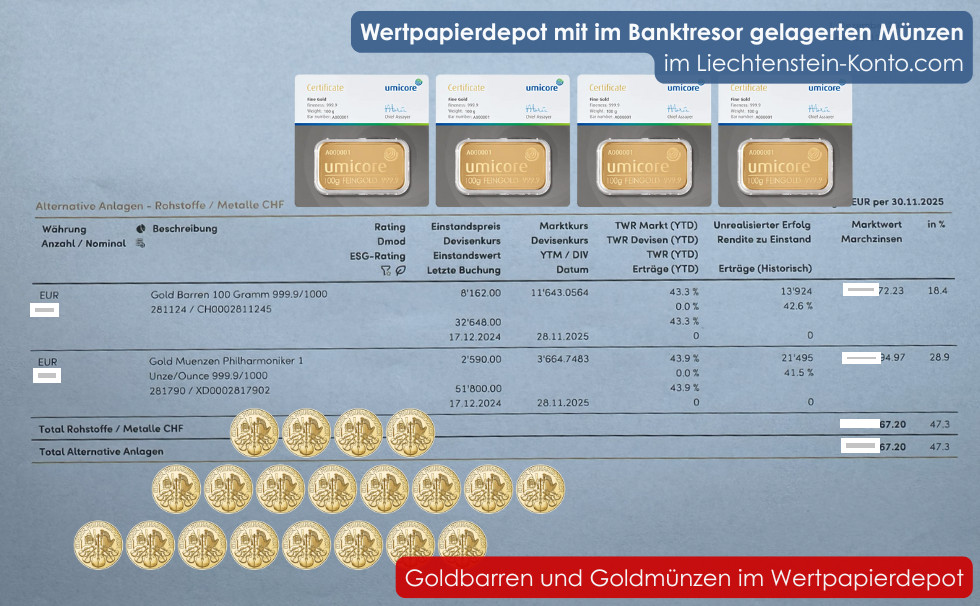

If there is still gold “to be bought”, it does not necessarily have to be done via the stock exchange. Gold bars and bullion coins in various sizes can be bought directly at fair terms from the partner bank and stored in the bank vault. The purchase is settled via the account, and the bars and coins appear on the securities statement!

Bars and coins each have an ISIN. Fascinating, right?

If investment gold has been held for a longer time, it can be delivered to the bank vault in Liechtenstein. This has advantages and disadvantages. The advantage, of course, is that this gold is pledged as collateral for new money. Instead of lying unproductive in a safe deposit box, fresh money can be obtained at low interest, which can then be put to work.

The disadvantage is that this gold becomes “visible” to a limited extent. It appears in the securities statement once deposited in the bank vault. Advantageous in this respect would be the simultaneous documentation for tax-free treatment after a holding period of one year and the clean sale to the bank. However, it is no longer a silent, discreet reserve known only personally. This must be weighed up. The pleasant aspect is that with one of the Liechtenstein banks there is, in fact, the opportunity to store existing gold in an orderly manner and use it as collateral.

Gold holdings: delivery into the bank vault and showing up in the securities account is possible!

Many common investment bars and coins can be deposited. Inquiries regarding own holdings are welcome. Denominations from 1 gram or from 1/10 ounce are possible. This is a special feature!

Regarding 3.) Credit line: absolutely inexpensive and discreet

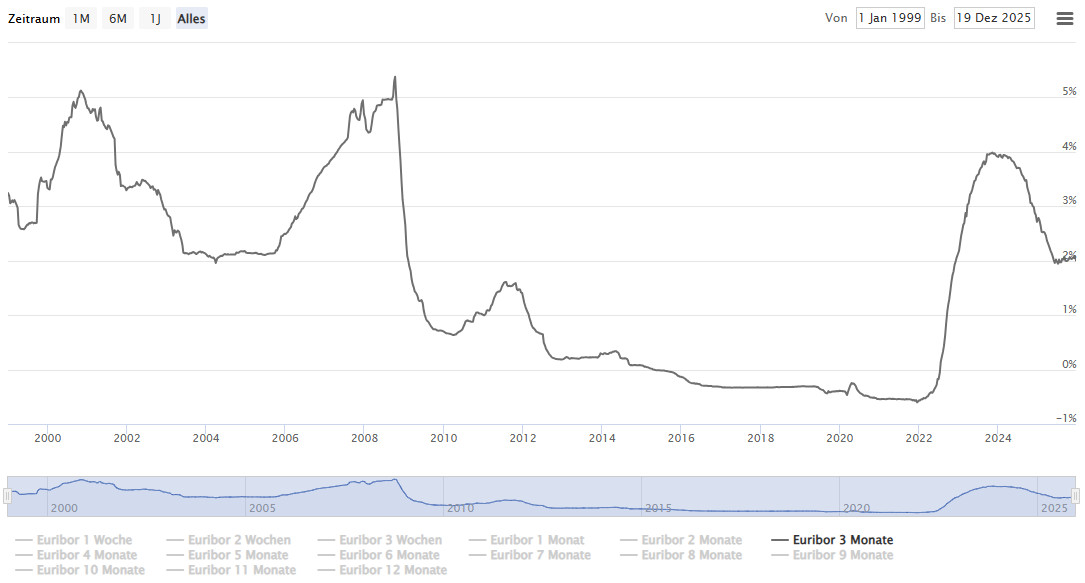

The bank’s margin is a maximum of 1.25% interest. When this great strategy was first reported 5 years ago, there were still penalty interest rates from the ECB and on many German call money accounts. Anyone who knew the right people and had sufficient creditworthiness could borrow money for less than 1%.

The system is still the same. Only now the central bank charges interest again, and lending between banks overnight also costs money. The key rate for banks in euros is the Euribor, and for this strategy the 3-month Euribor. At the time of publication it fluctuates around 2%. Adding the bank’s margin, the worst-case loan interest rate would be around 3.25%.

Only around 3.25% for capital available at any time! In addition, interest is charged only on the amount actually used and for the days it is used.

Historical interest rate development

For those objecting that interest rates could change: the development of interest rates since the introduction of the euro. Now just add the bank’s margin. Source: Euribor Rates.

If there is interest in working together, it is helpful to outline the plan and scale. It might be possible to negotiate the margin to below 1%! That would mean a current interest rate with a 2 before the decimal point!

Another important aspect: this arrangement is not visible to other banks! In Germany, current accounts, credit card limits, overdraft limits and even securities-backed credit lines are reported to Schufa. Loans of all kinds anyway.

The Liechtenstein loan is invisible!

The Liechtenstein bank will never report customer relationships to Schufa. Even if equity for property financing in Germany or in Florida – as some readers do – is organized via pledging gold in Liechtenstein, the other bank will not see this. Advantageous?

The gold or other assets such as shares not only remain personal property and continue to generate dividends in the case of shares, they are also held more securely in Liechtenstein. Access to assets from abroad is almost impossible, except for the owner or an authorized representative.

Regarding 4.) Making money with it

This point lies in personal hands. If there is a typical preference for call money and fixed-term deposits, the assessment will likely be: it is not worth it and there are certainly risks. Gold could fall in value. Interest rates could rise. Profits would be taxable. The excuses for remaining passive or staying within the usual framework are as numerous as they are varied.

The advantage: the credit line does not have to be used. It can be set up and left unused as a reserve. Essentially as an emergency credit line. But once a lucrative opportunity arises, there is immediate financial room for maneuver.

Just imagine: In the neighborhood, a very nice house is offered at half price due to some personal catastrophe. Naturally, there are several interested parties. However, everyone first needs to go to their bank and request a financing calculation or similar. It is possible instead to say: Please arrange the notary appointment, the purchase is made. Here is proof of capital.

In the USA, such buyers are known as “cash buyers” and they are preferred in 99% of cases and receive the deal. Whoever can pay immediately is king. Whoever needs three weeks with a bank to obtain a financing commitment is at a disadvantage compared to a financially prepared prospective buyer.

In this case, it is the renovation of a historic building that was quickly and relatively cheaply acquired as a cash buyer. If desired, an occasional update can be given. The instantly available and discreet Liechtenstein credit line is one of the secret tools in the financial toolbox.

This ensemble of buildings was acquired on short notice before coming onto the market. In such a situation, it is only possible to seize the opportunity if there is preparation. Setting up an invisible credit line based on assets is ideal preparation. Particularly for self-employed individuals and entrepreneurs, who otherwise often have a hard time with banks!

What might it be in your case?

Depending on the financial or entrepreneurial playing field on which you are active, the word “property purchase” can be replaced by something else. For example, business shares. There are people who buy shares on credit when they suddenly drop in price. That has already been done. Or company shares in a GmbH. Parts of business equipment from an insolvency or at an auction. At an auction, it is usually only necessary to show capital or pay a small deposit. When the bid is accepted, the entire amount has to be transferred promptly.

When cooperation is successful, the financial setup will soon be expanded. 😉 Think bigger!

For Florida friends it could …

… be the down payment for the holiday villa – without selling existing assets. The remaining part of around 70% is financed through US banks. Both parties know nothing about the other bank in the background. It is important to be invested in real assets in the medium and long term. Cash flow must be kept in view.

Could that be something? Has the book tip already been read?

Use monetary assets to acquire real assets

Offer

There is a chance to receive personal help in setting up the credit line, if:

- you are a pleasant character with whom it is possible to laugh on the phone

- 500,000 euros or more are to be transferred to Liechtenstein (alternatively a securities transfer or physical gold deposit is possible)

- a preliminary consultation is booked and the fee is paid in advance.

In this preliminary consultation, all questions regarding the smart setup of the credit line and account opening and use in Liechtenstein private banking are answered.

If the answers and instructions are satisfactory and it all seems to be a good fit, then a personal letter of recommendation to the bank is prepared. Which bank in the portfolio this will be becomes clear in the discussion.

Personal letter of recommendation and ongoing support

Since 2009 there has been extensive interaction with and experience of Liechtenstein banks and asset managers. It is safe to assume that there will be navigation to where the fit is best. This article merely shows a small section of the wide range of possibilities.

And yes, there are also solutions for 1 million euros and above in Liechtenstein and for from 5,000 or from 50,000 euros. The low-cost variant is by e-mail and does not include an invisible credit line. Nonetheless, a Liechtenstein account in the portfolio may be important when part of the assets are to be “moved to safety”, which is why the experience will be shared.

The greatest satisfaction comes from helping someone build something big. Therefore, there is particular joy about inquiries above 500,000 euros with physical gold deposit or securities transfer as well as raising fresh liquidity via a Lombard loan. This is invisible to other banks (= no Schufa entry) and therefore very suitable for further investments.

Closing words

The financial system is sick. And yet it works. Due to increasing state intervention, it works in a distorted way. This is not good for society as a whole. But it is possible to play with it and use it as it is. There is no change of the system. There is no manipulation of it, as politicians do. There is no change to personal advantage. It is used to personal advantage under current conditions.

The game described in this article is simple: parts of long-term stable assets are deposited in a much safer foreign country with a much safer bank. Depending on how it is invested, it will grow in value more than the cost (interest) of the fresh money obtained via the credit line.

In times when currencies are losing more and more of their value, it makes sense to be invested in real assets. So why not use the storage of real assets to borrow additional currency money in order to invest in real assets? What would be the investment of choice if fresh, cheap money could be obtained quickly?

There is gratitude for the people that could be met, appreciated and accompanied in this way. Now there are resources available for new ones.

Leave a Reply